At Tekaroid, we spend a lot of time looking at how systems quietly reshape behaviour. Not through force, but through design. Few changes illustrate this better than the rise of delayed payments. What began as a financial convenience has evolved into a behavioural reset, altering how people perceive money, responsibility, and risk.

The separation of spending and pain

For most of modern history, spending and payment were tightly linked. You handed over cash, watched it leave your wallet, and felt the cost immediately. Even credit cards preserved some friction through monthly statements and visible balances. But, delayed payment systems break that connection.

When the act of buying is detached from the act of paying, the psychological cost of consumption drops sharply. The purchase feels lighter. The decision feels reversible. Responsibility is quietly shifted to a future version of yourself.

This is not accidental, behavioural economics has long shown that people heavily discount future consequences. Delayed payments take advantage of this bias, turning it into a business model. The result is not reckless spending, but unnoticed accumulation.

From financial tool to behavioural habit

Delayed payments were positioned as solutions for exceptional purchases. Like larger or expensive items, with planned flexibility. Today, they are embedded into everyday consumption: Groceries, clothing, subscriptions, digital services, even minor upgrades are increasingly offered with deferred payment options.

The line between necessity and indulgence becomes blurred when everything can be postponed.

The problem is because this changes behaviour. Consumers stop asking whether they can afford something and start asking whether they can delay it. Budgeting shifts from managing money to managing timelines. Debt does not feel like debt as long as it remains fragmented.

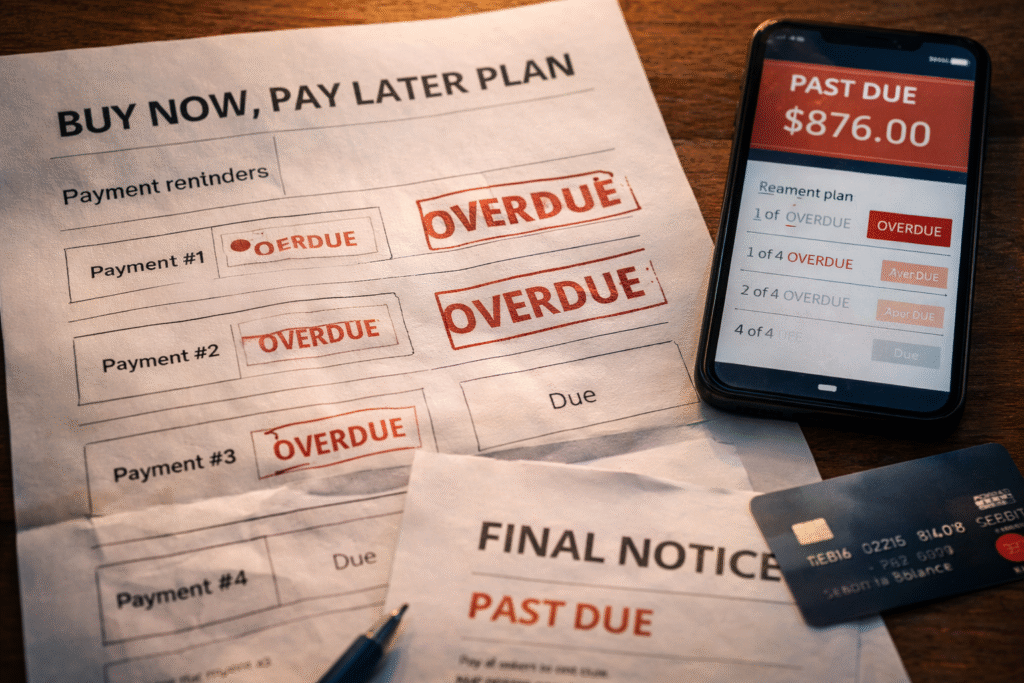

When debt no longer feels like debt

One reason delayed payments spread so quickly is that they avoid the emotional weight traditionally associated with debt. There is no loan application, no interest rate displayed upfront, no moment where the word “debt” appears clearly on screen. The transaction feels clean, almost harmless.

Psychologically, this matters. People are far more comfortable managing several small future obligations than one large present cost. A purchase split into four payments feels manageable, even if the total amount is identical. Fragmentation reduces perceived risk.

What changes is not income or lifestyle, but perception. Money stops being a fixed resource and becomes a flexible timeline. As long as the present feels affordable, the future is treated as negotiable. Over time, these pending costs stack quietly in the background, rarely triggering alarm but constantly shaping financial decisions.

Why financial stress feels permanent

One of the most striking effects of delayed payments is how they normalise background anxiety. When multiple future obligations are stacked across weeks and months, financial pressure becomes constant but undefined.

There is rarely a crisis moment. Just a lingering sense that money never quite catches up. This explains why many individuals feel financially strained despite stable income and moderate spending. The issue is not overspending, is the cumulative debit from deferred decisions.

Delayed payment systems do not create financial stress. They distribute it evenly over time, making it harder to identify and easier to accept.

The invisible weight of future commitments

Delayed payments rarely feel threatening on their own. Each obligation appears small and controlled. The effect emerges only when these commitments begin to overlap.

Instead of a clear financial problem, people experience a gradual loss of flexibility. Decisions become narrower. Options feel limited even when income remains stable. This creates a sense of constraint without a visible cause.

Because no single payment stands out, attention is never fully triggered. There is nothing dramatic to react against. Financial pressure becomes ambient, shaping behaviour quietly rather than demanding action.

This changes how people relate to money. Planning shifts from intention to reaction. Choices are made around what remains available rather than what is possible. Over time, this reduces confidence and makes long-term thinking feel less accessible.

Delayed payment systems do not announce their influence. They operate in the background, subtly redefining what feels affordable and what feels risky. Their impact is not immediate or obvious, but cumulative.

Design shapes discipline

The rise of delayed payments tells us something important about modern finance. Behaviour is no longer shaped primarily by education or discipline, but by design. When systems reduce friction, people use them. When costs are delayed, responsibility shifts. And when these patterns become normal, can lead a financial problem.

People stop experiencing financial moments as clean starts. Each month feels partially inherited from previous choices. The future is no longer open; it is negotiated in advance.

This matters because financial wellbeing is not only about numbers, but about psychological breathing room. When the future is always spoken for, even modest decisions feel heavy. Not because they are unaffordable, but because they arrive late.

At Tekaroid, we are less interested in blaming consumers than in understanding the structures that influence them. Delayed payments are not inherently harmful. But they are powerful. And power, when left unexamined, quietly reshapes behaviour.

Discover more in our Finance center.